Reflections on Investing in Public Markets

Summary of My Recent Reviews on Life and Work #1

This is an article that has been on my mind for quite some time. A bit of background here - When I was a tech product manager, I developed the habit of conducting regular reviews and retrospectives of my life and work learnings. It began with taking routine reflections on new products and features - an intrinsic part of the job. Over time, I expanded the practice to my life more broadly.

This article represents a further distillation and summary of my recent reviews on investing in public market. The main goal is to help me reflect on longer time horizons. It would be even better if it could also provide some inspiration for you.

As I am still developing my thoughts on many of the topics covered today, please feel free to reach out if anything is unclear or if you have further insights. Thank you.

P.S. I occasionally update my thoughts here. Last update: May 2025.

Principles

Design your own game. Combine your unique characteristics, goals, and the environment that you live in to design your own strategy and ecosystem. Design a game you can win and find rewarding.

I touch on ecosystem design in my post What I Learned About Investing from Darwin.

Evaluation of your game design - Sustainable, Traceable, Cumulative.

Focus on the downside, and the upside will take care of itself. Downside risks take priority.

Focus on the process, and the results will take care of themselves. Otherwise, you will end up with nothing.

The core is not the method itself, but your own iteration and evolution of the methodology.

Intellectual honesty. Not understanding is far more common than understanding.

Process

To begin with - Persistence and execution in implementing process are as important as the process itself.

Research framework

The three legs of this framework: 1) Business, 2) People and Culture, 3) Valuation.

Three questions to ask yourself before making an investment: 1) If the company is private and shares cannot be traded for five years after purchase, would you still buy at today’s price? 2) What biases do you have, and how do they shape the decision-making process ? 3) Is my focus on owning the busienss or merely trading shares?

ALWAYS focus on a company’s (discounted) long-term free cash flow.

Action framework

Win rate and payout rate. Opportunity Cost.

Liquidity.

Portfolio risk management, exposure to various risk dimensions.

Framework for opportunities to buy/add

Macro issues: Global financial crisis, European crisis - easiest situations to act.

Industry issues: Upstream / downstream cyclical issues. E.g. rising commodity prices squeezing margins.

Company issues: Evaluate if the team can address its problems. Each case requires specific analysis.

Framework for situations to exit/trim

Realizing the investment thesis is wrong.

Hitting target price / thesis plays out. VERY difficult situation, especially for high quality business, usually requires some buffer to hold. Focus on the long-term upside and stay aware of other opportunities as well.

Better investments available.

Portfolio risk management.

Framework for understanding abnormal share price movement

Structural reasons. E.g., addressable market, market concentration.

Rhythm reasons. E.g., impact of Covid on industries and business.

Valuation reasons.

Long-term capital returns of business are determined by two factors

Business nature. Whether the business has created value for users, generated user stickiness, and achieved economies of scale.

Market concentration.

Non-obvious Common Sense

On Edge

Understanding and acknowledging one's ignorance in 99% of cases and avoiding it. Being candid and admitting that one cannot answer most questions.

Fit provides the greatest edge. "How I differ from other investors/funds" may not be the right question to ask. Differentiation should be the result, not the starting point. The right questions are "What are my characteristics?" and "Given my characteristics, how should I design my game?".

On the other hand, rather than pursuing a differentiated portfolio and rare names, what matters more is the judgment and actions taken throughout the investment journey on the same names. It is the ability to make informed decisions and respond to risk events that holds greater significance. Even with the same holdings, over time, these factors can lead to significantly different choices and divergent outcomes.

Price discipline. Great companies also need to be owned at a reasonable price to achieve good returns.

Continuous learning in investing and life.

On Patience

Patience is an edge, but not every investor possesses it. For fundamental investors, patience is a scarce ability, but crucial for good returns. This includes patience in waiting for entry opportunities, patience in holding, patience when cash is abundant but good opportunities are scarce.

For great businesses built by great entrepreneurs, it is rare for all factors to perfectly align for an investment. Thus patience is an indispensable quality for investors.

Furthermore, discovering is just the first step, being able to hold and ride through is the core of returns.

On Persistence and Flexibility

Investment strategy and style should adapt to different environments, but the difficulty is that not every investor/fund can accommodate multiple styles, and be agile in capturing environmental changes at the same time.

Understanding the boundaries of one's strategy - When you sense the environment changing, and your investing toolbox is no longer suitable, self-honesty and courage to admit the fact are needed. Be agile in capturing environmental changes comes first.

Accommodating multiple styles requires maintaining an open mindset, avoiding path dependence (over-reliance on historically successful strategies), and continuous trial and error within controllable risks. Having your own style but also being open to integration and evolution.

The core is not the method itself, but your own iteration and evolution of the methodology.

On Time and Energy Management

Researching a company is not about more time spent equals more detailed research being helpful. The key is researching the critical questions (more effort is definitely helpful but with diminishing returns, also, be mindful of confirmation bias), e.g. in order to discover what a puzzle (if it is a dragon) is - the core is piecing together the dragon's surroundings, not other parts.

Spending time and resources on researching great business, rather than business at a good valuation.

Focusing on historical data that spanning many years (rather than spending time predicting the future) comes first. The importance of this is often under appreciated.

I don’t need a new investable idea every month / quarter / year. Continuous learning from great business in depth is more valuable than broad exploration.

On Portfolio and Risk Management

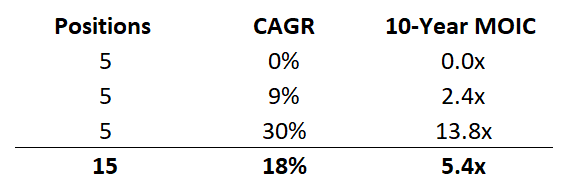

If you are skilled at finding rapid, durable compounders in your market, you can still afford to take a lot of zeroes and still compound at a powerful rate.

15 stocks portfolio, 1/3 go to zero, 1/3 compound at 9%, 1/3 compound at 30% In addition to industry and geographic diversification, another dimension of portfolio diversification worth paying attention to is diversifying the core thesis of each investment as a factor, such as how much portfolio exposure has the core thesis of a certain region's ecommerce penetration increase.

Facts, Opinions and the Mechanism behind

Facts are hard to change, but expectations are easy to change.

Facts are absolute. Opinions are relative. Everyone has their own interpretation of the facts, their own opinions.

The market chooses information, not information that determines the market.

Funds as an Organization

For this part I listed three questions I am thinking about, for most of which I don't yet have good and comprehensive answers myself. Welcome to discussions.

Principal-agent problem in an investment organization - How to conduct ecosystem and mechanism design to better align analysts' and platform PMs’ interests with those of the organization?

The diseconomies of scale for organizations also apply to funds - As the size of an organization increases, the value contribution of each individual within the organization decreases, and internal friction increases. How to match the optimal organizational size with your game design, and what methods can to some extent counteract the diseconomies of scale for fund organizations? I believe these can generate important organizational competitive edge.

How to cultivate the team's ability to think independently and maintain their own differing views through organizational mechanisms?

Life and Investing

Life is not just about investing, it also encompasses family, friends, community, how to navigate relationships and etc. Your approach to investment game design and objectives should fall within a broader life framework. You need higher-dimensional guidance. Establish your own way of perceiving the world and interacting with it.

The character of each investor determines the sets of opportunities they can capture and those they are destined to miss. Of course, one do not need to capture every opportunity. No one can seize every opportunity.

Be honest with yourself, making mistakes in life and investing is normal, can you honestly correct them.

Independent thinking against consensus and authority and curious attitude in life and investing.

As always, thanks for your reading and I hope you enjoy it. Stay safe and see you next time.